Digital payments made through credit cards are becoming more common—they offer several advantages over conventional payment methods. They are incredibly well-liked because of their convenience and security in making payments.

One of the most compelling aspects of credit cards is the variety of perks they provide to cardholders. Using a credit card correctly and responsibly may help you save money on regular purchases.

A rewards credit card, such as one that gives you cash back, airline miles, or hotel points for your spending, maybe a great way to get more out of your money.

Consistent spending can rack up all of these benefits over time. High incentive returns, low annual percentage rates, and no annual fee are hallmarks of the most accepted credit cards.

Credit card rewards feature a wide range of perks and protections. The best way to make the most of one of these cards is to pay your bill in full every month and make the most of your rewards by optimizing your redemption options can help you get the best out of these cards.

Thinking about getting a rewards credit card—keep reading to learn about some vital considerations while evaluating your alternatives and maximizing your rewards.

Important considerations while choosing your rewards credit card

Selecting a rewards credit card whose benefits are compatible with your spending patterns and budget is the most critical step in getting the maximum out of your card spending. While applying for a rewards credit card, consider the following aspects.

Rewards and cashback offered

A credit card’s cash back and other perks may significantly improve your shopping experience. As an incentive for customers to make purchases with their credit cards, most credit cards come with perks and rewards programs.

You may choose from various incentive schemes with a decent credit score. Airline miles, specific category spends, and cash back are just some examples of today’s many incentive schemes.

Currently, you may find cards that provide cash-back rewards ranging between 2% to 6% on certain purchases—however, these enticing offers come with quarterly or yearly spending limitations.

A credit card with cashback is a secured credit card that earns cash-back rewards for spending. The best cash-back credit cards are ones with a high rewards rate and low fees and interest rates.

As a rule, cash-back credit cards provide the most attractive discounts. These cards give you a rebate on a specific proportion of your purchases. Benefiting cash back rewards are excellent, but only if you keep your monthly payments current and complete.

Quality of your credit

Get your credit score before applying for a credit card since lenders use this information to determine the conditions of your card—whether your credit is decent or exceptional, a FICO score of 690 or above is required for rewards credit cards.

With a few exceptions, rewards cards typically demand excellent credit scores. You should check for inaccuracies on your credit report and fix them if your score is lower than expected.

The minimum credit score required for a particular card is often listed on comparison websites for such cards. You may narrow down your options for credit cards by consulting your credit score.

Avoid wasting time applying for a credit card that you know you won’t get accepted for. When you apply for a rewards credit card, the issuer will request your credit report. If you apply for too many cards at once, it might lower your score.

Your reward system is in line with your spending patterns

Identifying your spending patterns is the first step in selecting and applying for the most suitable rewards credit card for your financial position. Knowing your spending patterns is essential to getting the most out of your credit card rewards.

Pick a card with a more considerable earning potential in grocery and petrol spending if you make those purchases often. If you frequently travel, for instance, it may be worthwhile to apply for a credit card that offers bonus points or cash back on airfare and hotel stays.

A flat-rate cash-back credit card might be ideal if you don’t tend to spend much in any area of purchases.

Avoid carrying a balance

If you pay your monthly bill in full, you may avoid interest charges on your purchases. The APR (annual percentage rate) determines how much interest will be charged on a credit card balance. If you carry a balance on a rewards credit card, the value of your benefits will likely be nullified by the interest you pay.

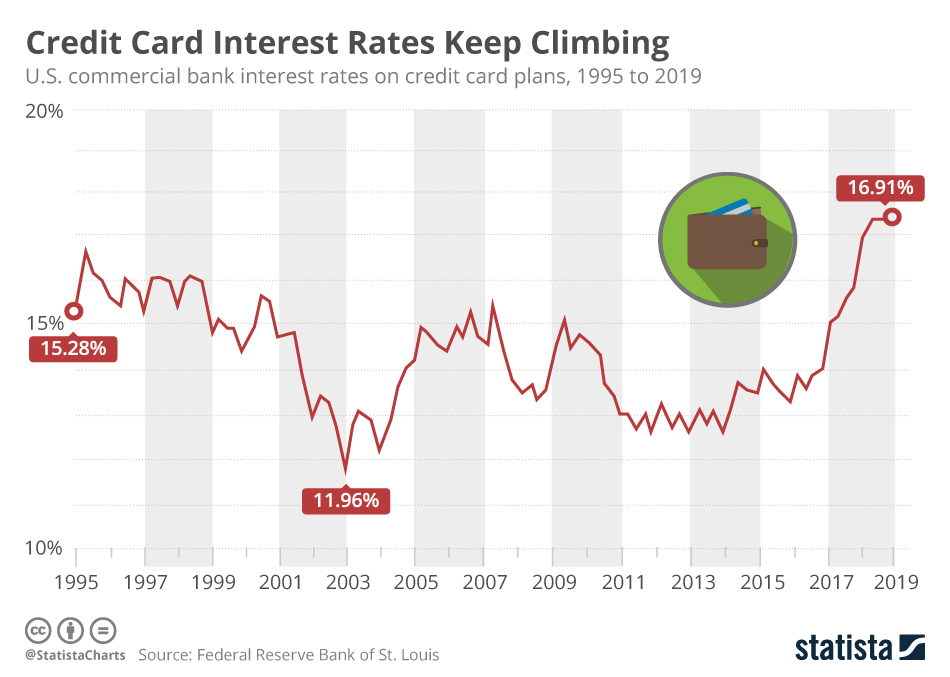

If you plan to cycle a balance periodically, a card with a possibly low-interest rate might be ideal. To provide some perspective, the typical credit card interest rate is about 16%.

Try to get a card with an introductory 0% APR period if you intend to use it for a large purchase that you can pay off in installments. Similarly, some balance transfer credit cards provide an introductory 0% APR on balance transfers for a specific time frame.

Check out the interest rate

Credit cards function as short-term loans at zero interest when paid in whole and on time. This grace period often lasts up to 50 days, giving you 50 days from the first day of your billing cycle to make a payment without incurring any interest.

Several credit cards offer enticing 0% interest promotional periods. This may seem like a beautiful bargain, but if you fail to make your payment by the due date, you will be charged the increased interest rate on your credit card. And it might increase manifold.

Always check the regular interest rate before applying for a credit card, not just the introductory one. Try to find the lowest interest rate for which you are eligible before making a final decision. It will result in saving you a lot of money.

Other considerations:

- A good credit score indicates responsible financial habits. Avoiding borrowing too much and making payments on time is the most excellent method to qualify for reduced interest rates.

- Check both the introductory rate and the annual percentage rate (APR) you’ll be charged once the introductory period ends.

Explore your redemption choices

Credit card reward points may usually be redeemed in two ways—online and through customer care assistance. Visit the card’s rewards site for further information on how to redeem your points.

Online redemption: Most credit card issuers now allow customers to redeem rewards, check balances, and request refunds online or via a mobile banking app. Following the on-screen prompts, you may redeem your accumulated credit card points for various rewards.

There are a few other ways that cash rewards might be disbursed, including:

- A credit on your card’s statement

- An electronic transfer into an existing bank account

- A paper check

The site will instruct you to cash your accumulated travel miles for free flights, hotel stays, and other perks. You may be able to redeem your points for cash, digital content, physical goods, or even contributions to a good cause.

Customer Care: For assistance redeeming points, you may contact customer care. There is usually a phone number you may call to redeem your points for anything.

The representative may provide details on your account, including the number of available reward points and the potential alternatives to cashing in those points. In addition, if you have questions concerning the point system or the typical reward processing time, you may clear them from customer service.

Remember that the value of your redemptions will vary with points and miles. For Instance— If you redeem your miles for airfare, you could earn one penny per mile, but products might only be worth 0.8 cents.

Some additional considerations

FTF and card acceptance

FTF (foreign transaction fee) might be associated with using your rewards card for transactions made in a foreign country. Foreign transaction fee is 3% approximately.

However, numerous credit cards, including many travel cards, don’t have this cost. It’s also possible that overseas use of your credit card may be limited due to the specifics of its payment network. Take these aspects into consideration.

Annual fees

Many consumers mistakenly believe that all credit cards include annual fees, which is not always the case. Annual fees may frequently amount to hundreds of dollars. The vast majority of credit cards do not charge a yearly fee.

Further, during the first year of card membership, the annual fee is sometimes waived for many cards that charge one. But certain credit cards usually come with a yearly fee—which may be eliminated if the cardholder spends a specified amount using their credit card in a year.

Thus, it is crucial to ensure you earn sufficient points from your card to cover these costs.

Wrapping up

A rewards credit card might be helpful if you have an above-average credit score and a healthy financial standing.

Users with the discipline to pay their credit card bills in full and on time every month while checking their credit card bills are accurate will reap the most benefits from the wide variety of rewards credit cards.

You may maximize your benefits if you know how to use a credit card wisely by charging as many of your purchases as possible to the card.